Editor's Note: Today, China controls between 70 to 90% of all rare earth metals on the planet, hinging the fate of our entire technological infrastructure on an increasingly-hostile foreign superpower that has already used its monopoly to punish its enemies. In small gestures, America and its allies have made efforts to re-secure resource independence, which the CCP attempts to thwart at every turn. The reason is obvious. In a technologically-advanced society, whoever controls the world’s supply of rare earth metals controls the world.

Ryan McEntush guests today with a primer on the topic. What exactly are rare earth metals, and why are they so important? What does it take to mine and process rare earth metals? How did we wind up in a world controlled almost entirely by China, and how do we free ourselves?

-Solana

---

Beneath the ancient sands of the Arabian desert, the fuel of our modern world lay entombed: petroleum, life itself condensed by time, which upon plentiful discovery would usher in a new era of industrial progress. It would also firmly shut the door on the fuel that once lit our society — whale oil. Accordingly, and perhaps in jest, it’s often said Saudi Arabia saved the whales.

This is how we like to think about history; a string of simple anecdotes weaving together to form our present. It’s nice! It’s also totally wrong. After a blitz of oil-driven industrial expansion, the discovery of massive oil reserves, which should have saved the whales, almost drove them to extinction. The problem with changing the world is it often changes in ways we can’t predict.

Today, the “save the whales” dream now centers on renewables, replacing fossil fuels with another revolution in energy, and beating back man-made global warming. Noble goals. Unfortunately, solar panels don’t grow on trees, and most of the materials and components we need to construct advanced technologies are controlled by a single, hostile, authoritarian country. Our rapid transition from fossil fuels to renewables is changing the world. But what does a carbon-free future controlled by China look like? And will it really be better?

To be clear, our goal should be the proliferation of carbon-free energy and a cleaner, better world for everyone. No one wants to kill the whales. But there are crippling second-order effects of this transition that we’re charging toward in blissful ignorance. Chief among them, if we don’t control our critical material supply chains, the path we’re accelerating down will lead to the end of American preeminence, and the global shift to a Chinese world order.

Put in simple terms, America and our allies lack secure access to the necessary materials for developing the next era of industry — not only solar panels, but key components of every machine in our entire technological infrastructure. Incredibly, we have given up our control of these materials by choice. Moral indignation and a sense of virtuous spite have driven us into dependence on what is clearly a geopolitical adversary, twisting us into a Chinese finger-trap. Now, as we slowly wake up and struggle, the grip tightens.

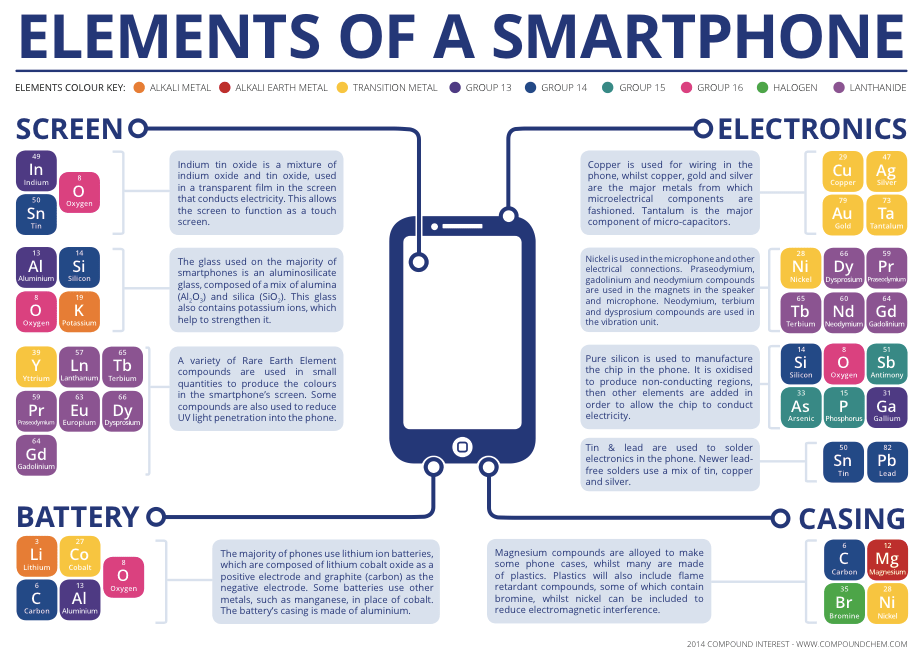

The situation we find ourselves in is fraught and complex, but it does begin simply with a straightforward question: what are the rocks in an iPhone?

Symbolic of the modern age, a smartphone acts as conduit for what is truly a marvel of industrialization — the computer. No longer do we write letters, read paper books, or go to a friend’s house just to chat. Today, a significant portion of our lives is mediated through technology. Consider our microwaves, speakers, and refrigerators, all covered with flashing lights and connected to the internet. Consider our vehicles, undergoing a rapid transition from gas to electric. Across society, analog technology is being replaced by batteries, and advanced instruments powered by electricity — in a perfect world, by renewables. This shift is especially dramatic in our most critical industries, including energy, manufacturing, and defense. Such incredible dependence clearly necessitates access to the valuable materials that are very literally the bedrock of modernity.

While there are many types of metals, there are a few that really demand your attention: lithium, cobalt, copper, nickel, manganese, graphite, and a group widely referred to as rare earth elements, or REEs. Even materials that we classically think of as mundane, like steel and aluminum, present immense risk to our way of life in the event of sudden scarcity. This goes much deeper than just iPhones.

At its core, this is a problem of chemistry. Not all metals are created equal. Let’s start with batteries.

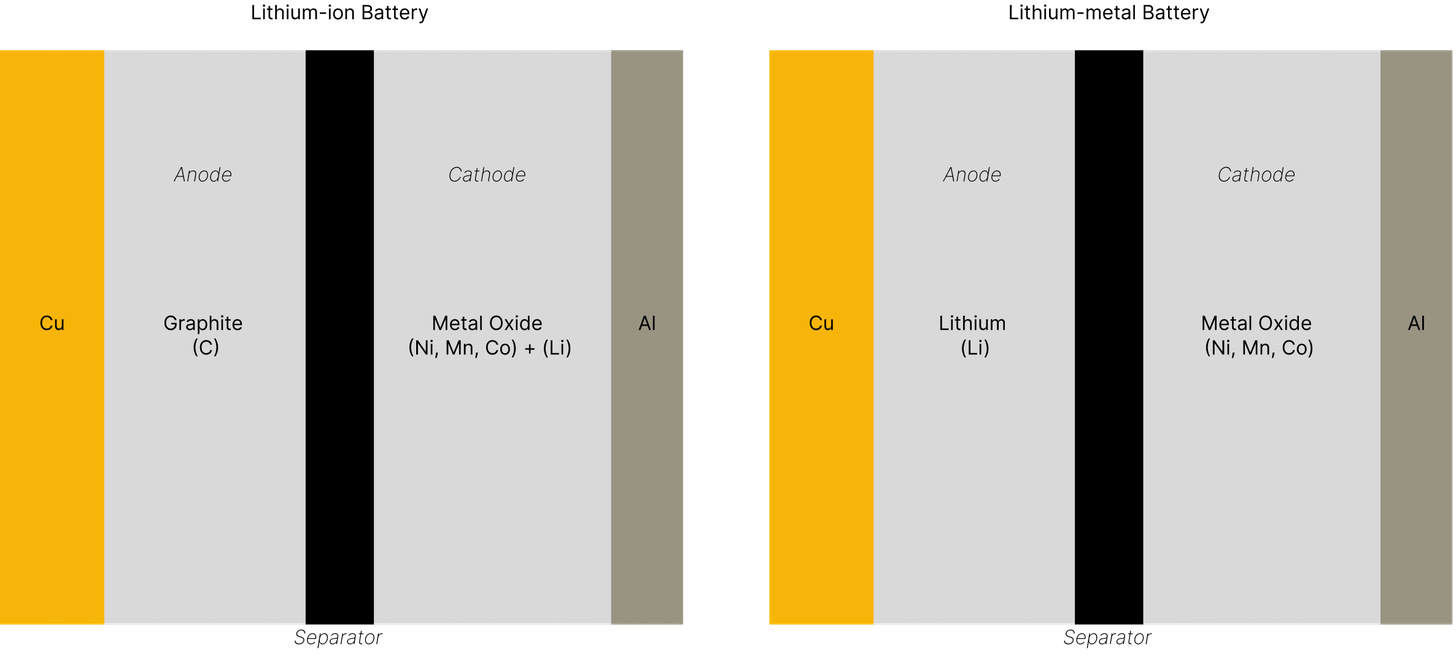

Today, any rechargeable battery is likely lithium-ion. This is what’s in your iPhone and Tesla. The reason for the dominance of lithium-ion batteries is quite technical, but most noteworthy is how batteries are quantified at the application level. Energy density, or the amount of energy stored per unit mass, is critical, and lithium-based batteries are the best we’ve got. Researchers remain committed to uncovering more advanced chemistry, yet are still largely working with the same components in varying combinations and structures. Lithium-metal batteries are particularly interesting given their even greater energy density, which at scale could bring us closer to things like electric planes or flying cars.

Consider the very simplified illustration below, and notice the change in anode.

Both the batteries of today, and those suitable to power the sci-fi future of tomorrow, are reliant on the same core group of minerals. It seems likely that as techniques for working with lithium-metal develop, new applications will be unlocked that generate increasing demand. The pursuit of advanced machines is an implicit desire for these materials. With our current technology, we can not escape this — it’s chemistry.

Like lithium, most people have heard of rare earth elements, or REEs, but may not fully grasp why they are so important, or to what they even refer. At a high level, the term “REEs” is useful primarily as a categorization for what might be further broken down into two groups of elements:

- Light REEs, or “Lanthanides”: Lanthanum, Cerium, Praseodymium, Neodymium, Samarium, Europium, Gadolinium

- Heavy REEs: Terbium, Dysprosium, Holmium, Erbium, Thulium, Ytterbium, Lutetium, Yttrium

It must not be understated how critical REEs are to much of what defines the modern world. As chemical catalysts, they are key to the processing of petroleum, both in industrial use cases and in catalytic converters found in gas-powered vehicles. Moreover, behind nearly every screen and flashing light you’ll find a mix of REEs, themselves emitting different wavelengths as well as making up the optical properties of advanced glass. These use cases are noteworthy on their own, but they pale in comparison to the fastest-growing application: magnets.

REE-based magnets provide a significant edge over their competition, so much so that they are now a cornerstone of nearly all aspects of advanced technology, including everything from computers, satellites, and cars, to medical devices, electronic motors, and aerospace instruments. Notably, these magnets are permanent, light, and incredibly powerful. The two most common types are neodymium and samarium magnets, lanthanides presenting unique advantages based on their specific makeup — often in combination with cobalt and plated in nickel. Hopefully, you recognize the pattern here.

The future will be powered by advanced batteries and magnets, but it will be largely supported by much more dull materials, like steel and aluminum. It’s estimated that 1 megawatt of energy generated from solar panels requires roughly 40 tons of steel and 47 tons of aluminum. With respect to wind, a 3 megawatt turbine requires roughly “335 tons of steel, 4.7 tons of copper, 1,200 tons of concrete (cement and aggregates), 3 tons of aluminum, and 2 tons of rare earth elements.” Beyond this, consider our ailing infrastructure and the sheer tonnage required to both retrofit and expand, much of which will be constructed with steel and aluminum alloys reinforced with nickel, manganese, or copper.

We live in a material world that requires, well…materials. In recognizing our reliance on specific inputs to build things, it follows that those who control these inputs have outsized leverage at their disposal. This is the nature of the trap we are in, and it becomes increasingly clear as we unpack the supply chains.

When it comes to these critical materials, there are three core steps to turning a rock in the ground into a usable, final product:

- Mining: extraction of a mineral ore from another, less valuable substance, like water, dust, or rock in the earth’s crust.

- Processing: refining mineral ore into pure, valuable materials.

- Manufacturing: using refined materials to produce batteries, electronic instruments, magnets, metal alloys, etc.

It’s through this segmentation that the Chinese finger-trap becomes painfully apparent.

Mining

To many, mining might seem like a rather abstract concept, mentally constructed by fictional renditions in video games or dystopian films. In reality, it’s one of the most important and sophisticated processes on the planet.

Mining typically begins with the identification of a mineral-rich vein. Historically, this was a “Eureka” moment of finding such a concentration that it literally leaked across the land and river beds. In recent times, ground-penetrating technology makes this easier, culminating in sophisticated machine learning approaches using magnetism, gravity, spectroscopy, and a variety of other data sources.

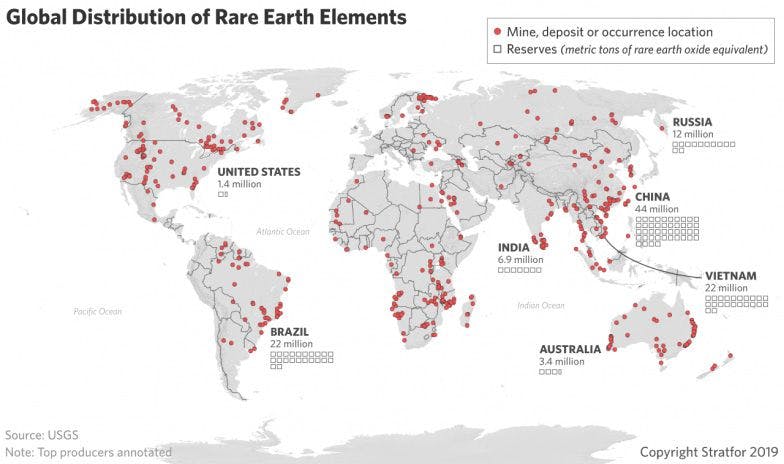

It’s important to note that even rare earth elements are not truly rare. They’re far more common than precious, but more familiar metals, like silver or gold, for example. But they’re distributed so broadly that it’s difficult to find concentrations high enough that make economic sense to mine.

While this graphic below only illustrates REEs, the trend of ore occurrence is directionally correct for most critical materials. As it stands, we are not mining, nor do we plan to mine, every known deposit.

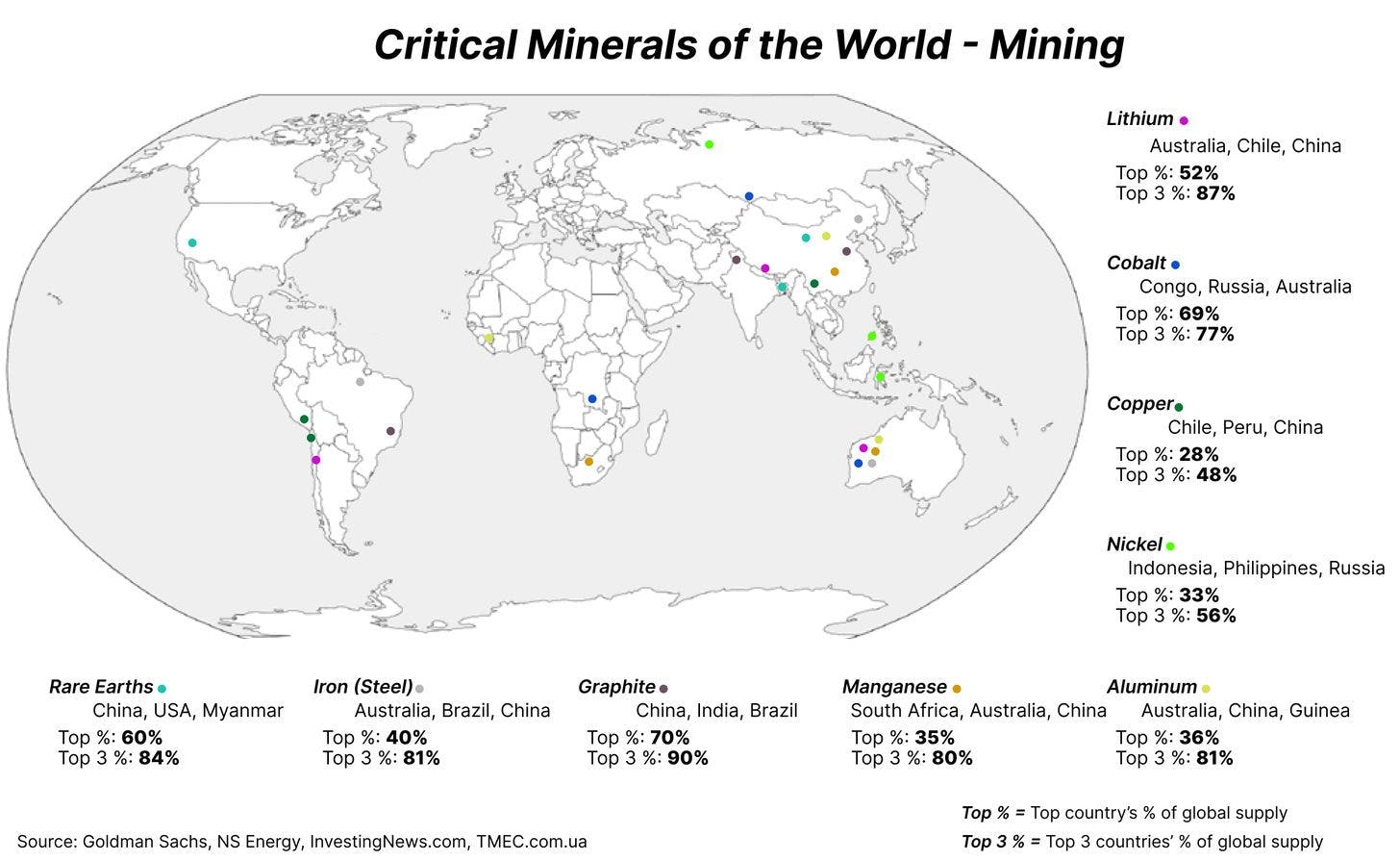

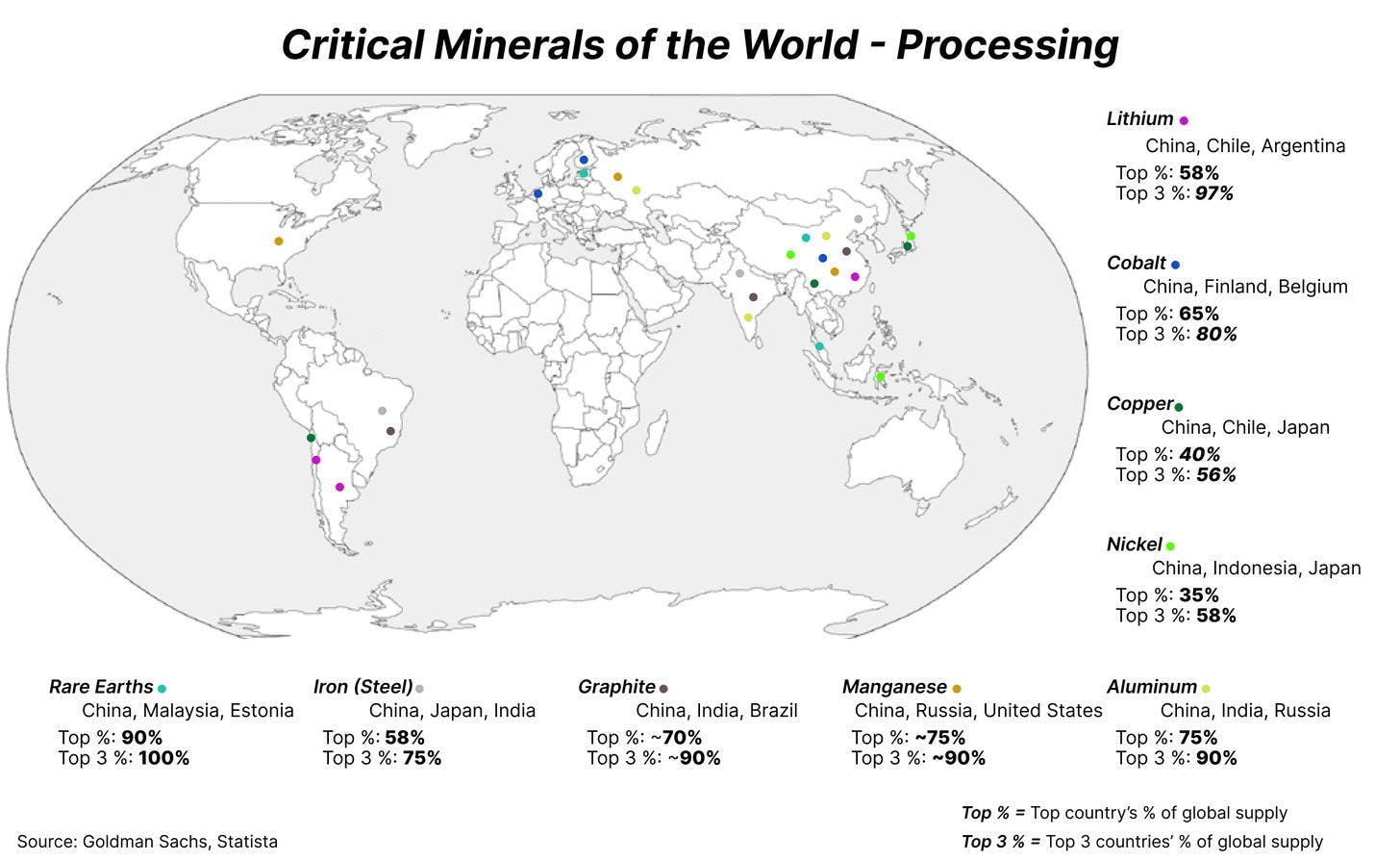

There are many reasons that would preclude mineral extraction from most deposits, including poor ore concentration, politics, or financial risk. This leaves a few major players with high market penetration. Consider the illustration below showing the mining sites of critical materials today. Specifically, I detail the % of global supply by the top mining country, as well as the % of the top 3 countries combined. Collectively, this data highlights a mineral’s relative mining concentration.

From a geopolitical standpoint, the most concerning mining concentrations are cobalt, graphite, and rare earths.

Cobalt, in particular, is infamous for its association with brutal labor practices at best and child slavery at worst. 80% of the Congo’s cobalt supply comes from industrial mines operated by international companies plagued with controversy, the majority of which are either owned or financed by China. Workers describe a blatant disregard for safety, including lack of proper equipment and procedure, that led to multiple fatal accidents in 2020 alone. The remaining 20% is extracted by what are known as “artisanal” mines, which is shorthand for small, local, and no regulation. Recent government efforts have attempted to consolidate this, but even so, the conditions are incredibly dangerous. It’s for this reason that companies like Tesla are sacrificing battery efficiency in an attempt to avoid cobalt entirely. Make no mistake, spare correction, the future will not be powered simply by advanced batteries, but by the blood of the Congolese.

Not to be outdone, the graphite mines of Northeastern China are like something out of a horror film. At night, it’s said that the air sparkles with tiny flakes of graphite floating aimlessly in the wind, blanketing nearby towns with a ghostly haze — roofs, water, crops, and spirits smothered by the detritus of “clean” energy.

Most notorious, and misunderstood, of all, we have rare earths. REEs are most commonly mined using a traditional open-pit method, though some compelling new studies suggest extraction directly from brine or the seabed might be viable. Shocking to some, the United States currently mines around 15% of the world’s REEs, owing to a single site in Mountain Pass, CA operated by MP Materials. This is certainly nothing to scoff at. Furthermore, recent discoveries in Wyoming and Texas, and internationally in Turkey, present an untapped opportunity to meet growing demand. Optimistic? Slow down. China’s dismissal of such discoveries is correct. If only simply mining critical materials was the problem.

Processing

Consider the global distribution of critical material processing:

China processes the majority of critical materials, and in the case of rare earths, virtually all of them. At its core, the reason for this comes down to convenience. Processing these materials is dirty work, especially if you want it done cheaply.

REEs are typically found in ore with a combination of other elements, requiring a multitude of filtrations and chemical baths to produce valuable oxides and purified materials — and isolating any radioactive waste. In China, this has historically been done haphazardly on-site, to a devastating environmental effect. Open pools of toxic wastewater are left to simmer across the rocky landscape, bleeding into nearby rivers and reservoirs.

For Lynas, a company operating an REE mine in Australia, sending raw ore to Malaysia for processing was the best option — that is until 2023, when they will be forced by the Malaysian government to do the dirtiest parts of processing in another country before shipping there.

Similarly, processing copper is a filthy, expensive business. At the Bingham Canyon Mine in Utah, crews “pull 150,000 tons of ore from the ground and process it down to just 820 tons of copper—barely 1/500th of the total.” And the remaining ~149,000 tons is what is known as tailings, or a mix of sulfuric acid, arsenic, lead, and cadmium from the surrounding rock. This stuff remains toxic for hundreds of years and demands special handling.

This speaks to a broader point and is illustrative of why China has the advantage that it does. They’ve largely ignored the environmental costs and safe, cleaner processes that other countries must follow, allowing them to work far cheaper and quicker. For example, as much as 50% of Chinese REE production comes from “illegal” facilities operated by gangs in southern China. However, recent crackdowns, aimed to control supply rather than protect the environment, have pushed production farther south into the Chinese-Myanmar border zone, making use of cheap labor and non-existent environmental regulations.

Regardless of how it is achieved, market dominance in mining and processing helps Chinese firms capture the greatest amount of value from the final stage—manufacturing.

Manufacturing

China’s consolidation of these supply chains manifests into being a dominant exporter of batteries, solar panels, and magnets, among other final products. Their superiority in manufacturing is no surprise, but for these components it is particularly concerning.

In the United States, we import 80% of our lithium-ion batteries from China. Notably, companies like Tesla source much of their supply from CATL, a Chinese firm that is the largest battery producer in the world. Even the Tesla “Gigafactory” sources the majority of its refined materials from China, and if these materials don’t arrive, factories falter. Furthermore, of the 181 massive-scale battery factories planned or already built, only 10 are in the United States—and 136 are in China. It’s easy to criticize American companies, like Tesla, for reliance on Chinese materials and components, but their choice is to begrudgingly accept this reality as it is today or not operate at all.

Tragically, solar panels, an iconic representation of clean, renewable energy, are nearly equivalent to blood diamonds. China produces 80% of the world’s solar panels, the majority of which are constructed in coal-powered factories with slave labor in the province of Xinjiang. President Biden has since blocked a large supplier from exporting to the United States, though research suggests this issue is systemic in China and truly requires a full cut-off.

Similarly, China’s extreme dominance in rare earths extends deeper when we consider the final products. Magnets, for example, are needed for pretty much anything that can be justified as advanced technology. Today, China produces 92% of the world’s supply; consider that an F35 Fighter Jet contains hundreds of pounds of these.

Remember MP Materials and the Mountain Pass rare earth mine? Why don’t we just make magnets here? Well, around 10% of the company is owned by the Chinese firm, Shenghe, which is also contracted to buy nearly 100% of their concentrates and oxides for processing. We aren’t building magnets here because, as of now, every bit of REEs mined gets sent directly to China. To their credit, MP Materials is looking to change this. Plans to build a magnet factory in the United States make me optimistic, though even at full capacity it will consume only 10% of Mountain Pass’ REE production, sending the rest to China. These are steps in the right direction, but we are playing catch up to what has been a long-term, global strategy.

And I mean this sincerely. Since the late 20th century, this has been a part of a strategy to exert international power through the control of critical materials and components.

“The Middle East has oil, China has rare earths.”

- Deng Xiaoping, President of China, 1992

Over time, China’s strategy has evolved into encapsulating all of the critical materials discussed above, increasing consolidation as you move downstream in their supply chains. This is an explicit two-pronged approach: the development of rare earth supply chains and the technology applications surrounding them.

Consolidation of lithium, copper, cobalt, nickel, manganese, graphite, aluminum, and steel are byproducts of a narrower ambition—simply, dominating production of final components like batteries, solar panels, and other industrial technologies. As new developments, like sodium-ion batteries, reach production scale, expect similar consolidation in those materials. It follows that the top exporter would also be a top importer of raw minerals, but, nonetheless, the outcome is a reliance on China that compounds as we shift further towards a more advanced, electrified world.

Economic theory would cause you to believe that any exercise of supply power would lead to price hikes and thus investment in competition outside China’s scope. This is true in free and fair markets, but this scenario is neither.

The Chinese Communist Party has ingrained itself across military, civil, and economic affairs. Over the last 50 years, this has become increasingly directed towards critical materials and emerging technology production.

This begins with the concept of “Two Resources, Two Markets”, a Chinese initiative focusing on protecting their own domestic economy while siphoning from the rest of the world. Naturally, this mercantilist-like philosophy is on display when it comes to critical materials.

Over the last decade, China has really ramped up these efforts. In 2011, the Strategic Emerging Industries Initiative identified seven technologies that would form the backbone of their industrial policy. Importantly, these were all made from critical minerals. Declared soon after in 2013, the Belt and Road Initiative aims to finance infrastructure development around the world, much of it designed with the parallel goal of ensuring energy and material supply chains. In 2015, the Made in China 2025 plan highlighted dominance in rare earths and high-tech manufacturing as key pillars. In 2020, China confidently stated the ambition of not just following another country’s product designs, but setting world standards in emerging technology by 2035. The trajectory here is clear and not surprising. But what’s concerning is how these policies are actually deployed.

In 1995, a group of Chinese state-backed investors, literally a part of Deng Xiaoping’s family, purchased a majority stake in General Motors’ rare earth magnet supplier, Magnequench. Within a few years, they copied their technology, forced the closure of the American factory, and moved production to China.

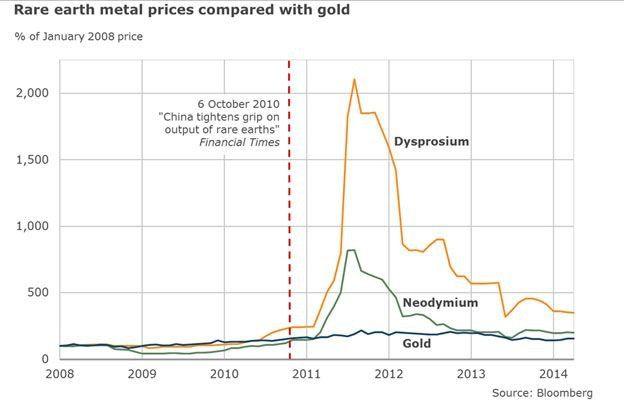

In 2009, the Ministry of Industrial and Information Technology developed a national export control strategy, a newfound power first demonstrated soon after. In 2010, conflict over the Senkaku Islands led to China cutting off Japan from REEs—a claim that Chinese authorities contested, yet lost in a dispute at the WTO. Naturally, China’s grip on supply shook market prices.

It was in this ramp up and sudden spike that investors flocked to Molycorp, the site operator of what was once the sole source of rare earths in the world—Mountain Pass, CA. Starting back up in 2010, the mine was developing new, cleaner processing technologies that were now viable in the current market. That said, after settling their WTO dispute, China flooded the market and forced Mountain Pass into bankruptcy. In 2017, this mothballed mine was purchased by MP Materials, which, as you know, has a Chinese state-owned firm as a large shareholder and its major purchaser.

In the years prior, China had consolidated their 99 domestic rare earth firms into 6 state-owned enterprises that operate as arms of the CCP with blank checks and little concern for finances. A “Go Out” strategy was sanctioned and firms began to invest in upstream mining and processing around the world, like in the case of MP Materials. But they are not alone. Projects in Australia, South Africa, Kazakhstan, and even Greenland are financed and have agreed to send oxides and concentrates to China. This is not a strategy that liberal democracies can compete against with capitalism alone.

Other critical minerals in advanced technology have not escaped Chinese clutches. Recently magnified by a formal Belt and Road Agreement, China has committed $9 billion in investments in the Congo in return for exclusive mining rights, a figure matching the entire Congolese government annual budget. Tianqi, a Chinese state-founded firm, has purchased significant stakes in lithium mines in Chile and Australia, providing effective control of supply towards their own battery manufacturers, like CATL.

This consolidation of critical material supply chains is a weapon. They tested it on Japan in 2010, then leveraged state capacity to strengthen their supply lines, and now, in recent years, have resurfaced this threat. In 2019, ignited by the trade war, China threatened to cut off REE supply to our defense industry. In 2020, they further centralized supply laws, and then in 2021, export controls were levied after weapon sales to Taiwan.

From a national security perspective, this is a major, and increasingly direct threat — especially as we shift away from fossil fuels, with a larger chunk of our economy, and livelihoods, dependent on materials and components that China controls.

What would actually happen if China embargoed Taiwan, the source of 90% of our high-end computer chips? How can America act when protecting our chip supply, and our strong ally, also compromises our access to other critical resources?

In many respects, this dilemma feels eerily similar to what has taken place between Europe and Russia. Clean energy champions in Europe have cut domestic production of natural gas, effectively outsourcing emissions—and with it, power. Slowing supply and triggering economic pressure was a crucial piece in the invasion of Ukraine. From this lens, it makes sense why Germany and Turkey, among the most dependent on Russian natural gas, have remained relatively indecisive compared to their contemporaries. Helping drive this reliance, Russian-state media, and Putin himself, decry fracking and regard it as being “terrible for the environment”, meanwhile their leaky pipelines continue to be a significant source of methane emissions. Some reports even link Russia to funding EU environmental groups directly.

Building off this example, China has been caught inciting protest in the United States over rare earth mining. While I don’t claim foreign interference to be a primary cause for our current environmental policies, one should probably assess their position if aligned with clandestine Chinese operations.

While downstream manufacturing growth has exceeded expectations, heavy regulation has held back upstream production, and, in some cases, has even outright blocked mines in Arizona and Minnesota. The Biden Administration has stated the goal of fixing this, but instead of proposing immediate changes to the current rules, initially written in 1872, the Department of the Interior created an “interagency working group”.

This appears to be, as some have reported, part of a broader political strategy to appease environmentalists and Indigenous groups. Under our current system, permitting is subject to a full gauntlet of regulations — the National Environmental Protection Act, Clean Air Act, Clean Water Act, Endangered Species Act, Administrative Procedures Act, as well as many other federal and state laws. A recent government report claims new facilities take on average two years to approve, if at all, though industry advocates argue that this process takes far longer, often closer to ten years. Democrat attempts to reform mining regulation have been met with blowback from more progressive groups, and industry advocates argue that proposed changes will only serve to stifle development when we need it most. Alternative efforts have been made and some politicians are speaking up, however I suspect we remain far away from an effective Congressional compromise.

Both parties agree that critical material independence is important, but no one has been able to make a difference, nor is it even clear who the central authority is on this matter.

In spite of this, Department of Defense support for MP Materials and Lynas is bringing back a domestic rare earth supply chain, and broader programs have been deployed for battery production. Successful actions, like these, stem from the military and are supported by national security concerns, while commercial projects are routinely inhibited by elected officials and the Department of the Interior. Progress, it seems, largely has come down to avoiding notoriously sclerotic institutions entirely. This divide within our own government impedes broad-scale development, and while we bicker, China laughs; CCP officials consider the United States’ critical material independence “wishful thinking”.

Protecting our environment and transitioning to clean technologies must be done, but we can’t ignore the tradeoffs. We are now moving from a world in which the United States was the top exporter of fossil fuels, at roughly 20% of the global supply, to a world in which China controls >75% of all the materials needed for nearly everything that defines modernity. No matter how badly some would like to ignore this basic fact of reality, someone has to mine, process, and manufacture the critical stuff with which we build and maintain human civilization, and we can’t just blindly offshore the responsibility to China — to whom we also cede the future. The world I want my children to live in is not just clean and beautiful, but free, and that is not a world controlled by the CCP.

The solution to a Chinese finger trap is to push inward before pulling out, and I believe this analogy holds true for the situation we are in. We must toss aside our foolish ideals and accept responsibility for a short period of toxicity; only then can we secure our long term future and innovate to build a cleaner, better world. The strategy to combat China’s dominance in critical materials can be broken down into two core components: offense and defense.

From an offensive perspective, we must encourage our own mining, processing, and manufacturing. This includes developments in mineral discovery, increasing yield from ore, cleaner methods of processing, and recycling. We must also re-shore battery, solar panel, and magnet supply chains, among other advanced technologies.

Unfortunately, the free market is not enough to achieve this. Tax incentives, permitting overhauls, grants, offtakes—these are all tools in our arsenal that the government should be employing. And not just in America, but across the globe. Defense programs should require 100% of their materials be sourced among Five Eyes nations and other key allies. To do this, we should leverage existing institutions, like the United States International Development Finance Corporation and the EXIM Bank, to finance investments in upstream mining and processing around the world.

Defensively, we must work to prevent Chinese state-backed enterprises from strengthening their existing global control. Frankly, it is ridiculous that our only rare earth mine can have significant ownership by a Chinese firm and be completely reliant on their purchasing. I understand that this is necessary for their financial survival, but this is a place I’d especially welcome additional government support. We also need to encourage CFIUS to be far more stern when it comes to blocking foreign investment in these critical materials. Of course, the CCP has done this all over the world, so this, too, requires working with our allies to block China’s tightening grip.

You’d think consolidating our own critical material supply chains would be something that we could all agree on. In a world where America accomplishes this, the China hawks weaken their enemy, labor movements get jobs, and, in reality, the climate activists get far greater control over the trajectory of global environmental damage. Moreover, we’d also not be actively supporting a regime that is threatening our allies and enslaving their own people. This shouldn’t be controversial.

It’s said when Faust approached the crossroads he met a devil waiting for him. Dissatisfied with his life, he made a bargain with the creature — his eternal soul for the world’s material pleasures. The deal seemed great at first, but, in time, it led to his damnation. At first glance, the lesson of the tale induces a preference for the eternal and immaterial. In truth, I believe it also tells us something far simpler — to treasure what we have over what we desire.

The United States has systematically traded our own critical material supply chains, once the envy of the world, in exchange for a lie. Out of sight and out of mind, we declare environmental and labor victories while outsourcing the ugly side of modernity to the downtrodden around the world, subject to odious forces beyond their control. Perhaps ignorance helps us sleep at night. Or maybe in our industrial self-immolation we feel pure and holy.

But once we awake from this fantasy world that we are in, we collapse into the physical one. A place of hard rocks that must be mined, processed, and manufactured into useful components. And that, in troubling times, might be used to engineer war machines to protect our people, our allies, and our liberal values. There is no such thing as a free lunch. It will be hard, expensive, and dirty, but if anyone can do it better, it’s America.

-Ryan McEntush